Sending Request.

Please wait...

Sign in.

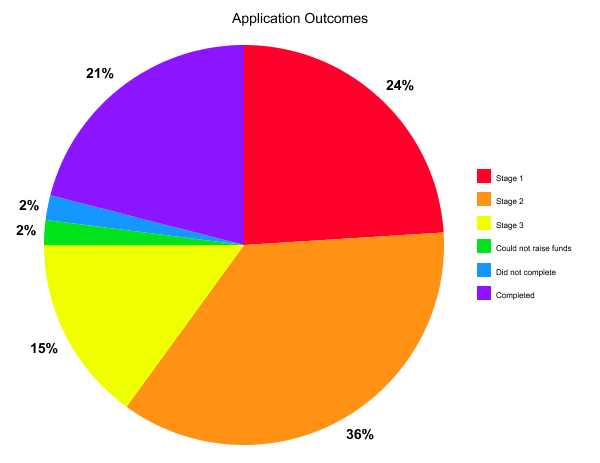

An application has to go through 3 distinct Stages prior to listing and it could be rejected for a number of reasons throughout this period. In the operations team we receive around 40-50 applications and enquiries a month and reject 79% of these. We only allow the strongest applications with appropriate security on to the platform.

We reject 24% of our applications in Stage 1. We filter out any application that does not meet our basic criteria (more on this below) and some applicants choose to withdraw at this stage.

In Stage 2 we gather all of the required information for the application including security information and accurate accounts. This is the longest part of the process as applicants often have to engage their accountants to make edits to their management accounts to bring these in line with our minimum standards and expectations. It is important to us that the accounts are presented to the lenders in both an accurate and comprehensible way. We have 36% of all applications rejected or leaving the process at this stage.

In Stage 3 all of the gathered information is passed to the underwriting team to ask questions about the accounts, assess the risk of loan and to determine its suitability for listing. 15% of all applications are rejected at this stage which represents 37% of the applications that make it to this stage.

The remaining 25% of applications make it to listing, where 2% fail to raise the funds, 2% fail during the completion process and 21% are fully funded and completed.

18% of our rejected borrowers are ineligible and do not meet our basic criteria of turnover, entity, UK based, profitable and able to provide the required accounts.

23% of those rejected meet our criteria, but are rejected by the underwriting team because they do not pass our risk model, or in some way are unsuitable for the site. This includes 6% with insufficient security, 4% where the loan is unaffordable.

When we receive a loan application, we take it through a number of checks and verifications, and a whole lot of scrutiny, before we allow it to be listed on the platform for your consideration.

These checks focus mainly on the business and its ability to service a loan at the likely rate that it will achieve on the site, as well as taking a look into the business’ previous trading history and the associated businesses linked to it through its directors and shareholders. Much of this information is driven by third-party data services, which use thousands of touchpoints to bring together a more comprehensive picture of the applicant’s business.

This information is then used in our bespoke risk tool, and the accounts supplied by the business are further analysed by our underwriters to ultimately determine a risk score between A+ and C. A business can fail in its application at any stage through this process; only 20% of the businesses that apply make it through to listing.

Aside from looking solely at the business, we go a step further and also look at the people behind the businesses. We take into account the businesses they are involved in, the businesses they may have previously been involved in, as well as their personal credit history.

We do this because we understand that many businesses are strongly driven to success – and sometimes, ultimately, to failure – by the direct actions of their directors and majority shareholders. What’s more, if a business does fail, any loans with a Personal Guarantee means that the directors may ultimately become responsible for the debt should the business fail to make its repayments. It is therefore important for us to know more about the directors and their personal financial history, and we do so by carrying out personal credit checks. This data is then used to further our assessment and risk of the business, contributing to the final rating.

Where a director has a poor credit score (or has adverse information), we aim to assist them with taking remedial action, however, an application may be declined on this basis.